Pay should not be attributed to the month of payment.

Pay components related to the month of payment neither should nor can be marked “pay attributable to another month”.

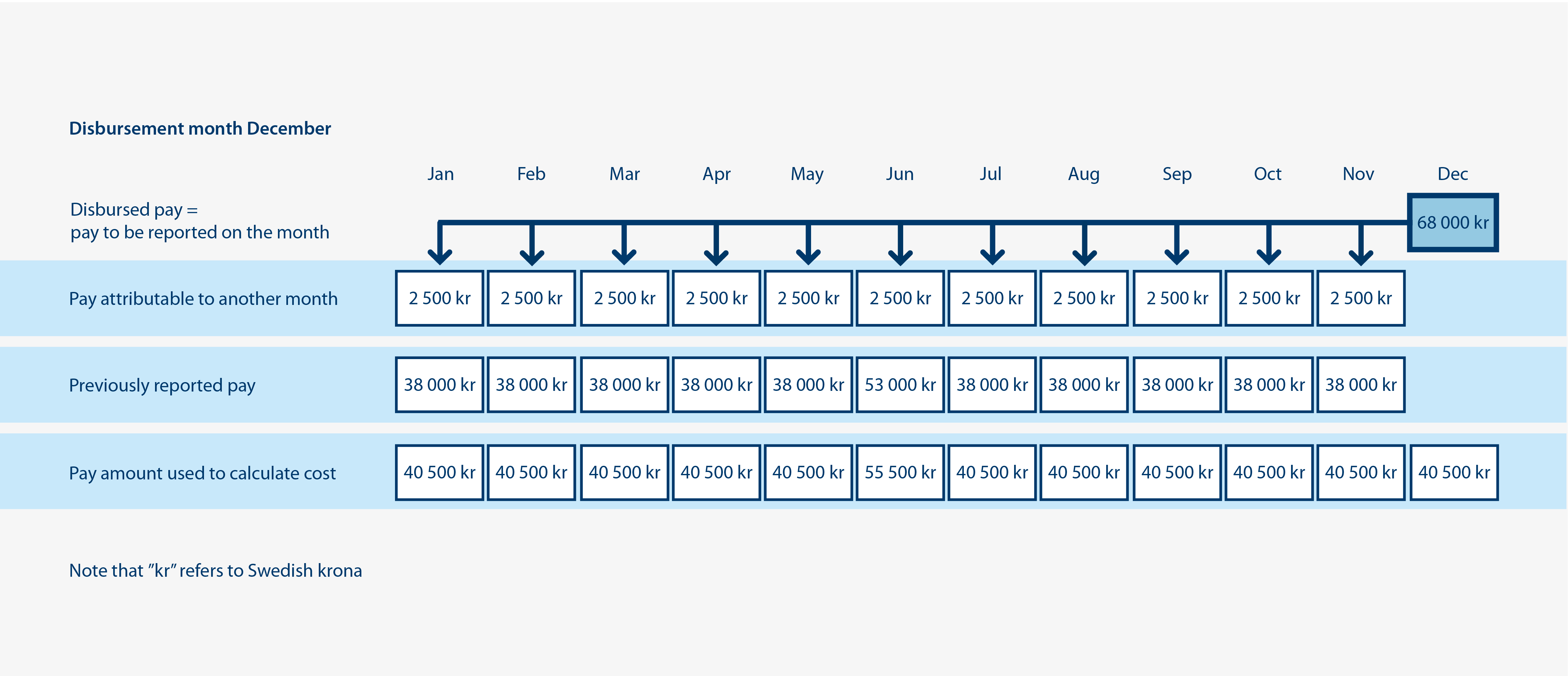

Pay cannot be attributed to a future month.

Salary payments for specific months should be reported – pay for months in the future can therefore not be reported.

The portion of the pay amount marked “pay attributable to another month” cannot exceed the total pay amount reported for the month.

It is not possible to attribute pay from the same payment month multiple times to the same month for the same individual.

If the paid salary contains multiple pay components to be allocated to one and the same month, add up the total amount to be attributed to that month and enter it.